Cimic tanks on earnings miss, but is the move overdone? (CIM, LLC) **Buy SH US**

WHAT MATTERED TODAY

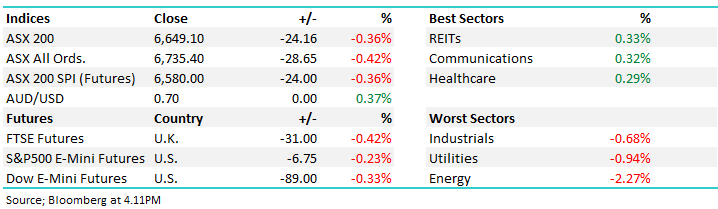

The market softened again today however overall it was another low volume session where a lack of buying interest rather than anything more sinister saw the index close in the red. Asian markets were weak, Japan the worst of the region down nearly 2% while US Futures tracked lower during our time zone.

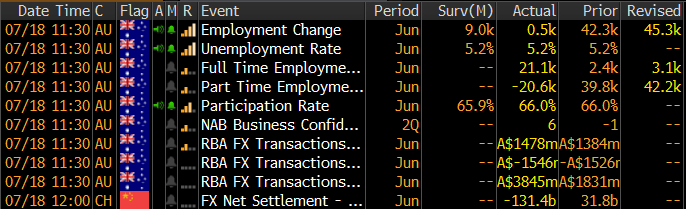

On the economic front today, employment data was in line with expectations (5.2% unemployment rate) on the headline number, however the composition of full time v part time jobs was strong.

Economic Data

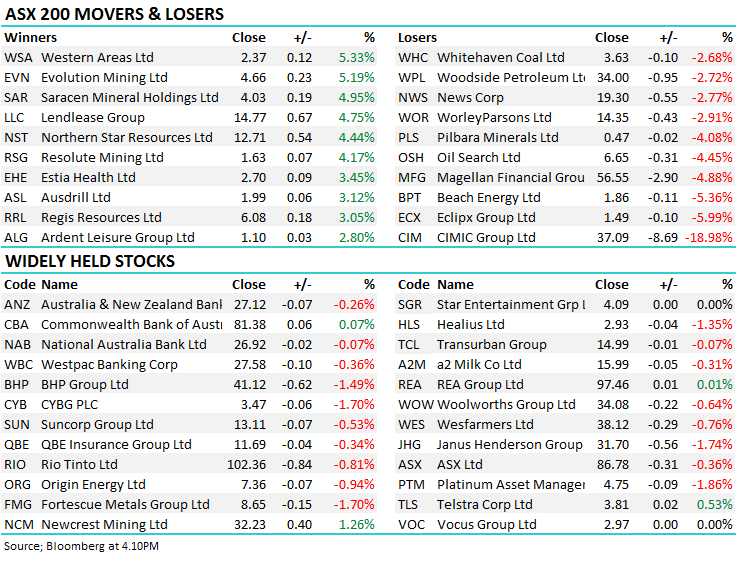

Energy stocks the biggest drag today following Crude’s decline overnight while a number of company updates caused some big moves in stocks. Nickel miner Western Areas (WSA) released a strong quarterly update and rallied +5%, a buoyant Nickel price also helped while Cimic (CIM) was a casualty on the downside dropping a substantial ~19%. Harry covers the stock below and thinks the selling is well and truly overdone, particularly given the reinstatement of the on market buy-back. Elsewhere, Alumina (AWC) was hit early, but recovered late following the quarterly report overnight from Alcoa while Estia Healthcare (EHE) recovered +3.45% after dropping 5% yesterday on the announcement of a class action.

We covered Domino’s in the AM report today and the stock did close higher – up by 2.4% - and for now we’ll hold our short term position.

Overall, the ASX 200 lost -24pts today or -0.36% to 6649. Dow Futures are trading down -89pts / -0.33%.

ASX 200 Chart

ASX 200 Chart

CATCHING OUR EYE;

CIMIC Group (CIM) -18.98%; shares tumbled to 2 year lows following a soft first half result which the company presented after market yesterday. The profit line was marginally better than 1st half 2018 at $367m with the company needing a large second half skew to meet the reiterated guidance of $790m-$840m. The miss was driven by the construction business which accounts for nearly half of CIMIC’s earnings. Much of the 15% decline here was felt in its Asian market where the company is facing backlash from alleged defects in construction works in Hong Kong. The tumble was offset by a surge in the mining division which saw profits rise more than 25% - a positive read through for our current holding is Ausdrill (ASL) which rallied by 3.12% to close just shy of our +$2 target.

CIMIC is used to seeing a marginal skew of around 45/55 to the second half earnings which would be enough to meet the lower end of guidance at the full year result. There is also a clear path to achieving this as total work in hand rose 6% in the half. The Australian infrastructure market – where CIMIC is the biggest player – has a solid pipeline for the next few years. The sell off today seems too aggressive given that it isn’t too far off the pace to meet guidance, and the company announcing it will recommence it’s on market buyback which should also be supportive. A weak result in a thinly traded stock on a low volume day = 19% decline. CIM is now back on the MM radar.

Cimic (CIM) Chart

LendLease Group (LLC) 4.75%; announced it has entered into an agreement with Google to build out Silicon Valley – estimated 15 million square feet of residential, retail, hospitality and other community uses in creating suburbs in the particularly under developed area. Work is expected to start in 2021, and pending approval would result in around $US 15b spend over the next 10 to 15 years in the San Francisco Bay area. This is the largest single deal LendLease has made in however it will be 24 months before works begin and plenty of detail still to be fleshed out.

LendLease (LLC) Chart

Broker moves; While UBS does not provide their research to Bloomberg (which is where the below list comes from) we see today they upgraded their price target on Bingo to $2.70, up +35% on the prior target largely on the back of positive earnings revisions following planned price hikes. We sold BIN recently and are now watching closely, there upcoming results remain the key.

- Cimic Downgraded to Underperform at Macquarie; PT A$43.80

- Cimic Downgraded to Underperform at Credit Suisse; PT A$35

- OceanaGold Reinstated at Macquarie With Outperform; PT C$5

- Syrah Downgraded to Underperform at Macquarie; PT A$0.90

- CSL Downgraded to Neutral at Citi; PT A$239.60

- Magellan Financial Cut to Underperform at Macquarie; PT A$45

- G8 Education Downgraded to Neutral at Macquarie; PT A$2.80

- OceanaGold GDRs Upgraded to Outperform at Macquarie; PT A$5

- GrainCorp Downgraded to Hold at Morningstar

- Cochlear Downgraded to Sell at Citi

OUR CALLS

No changes locally today.

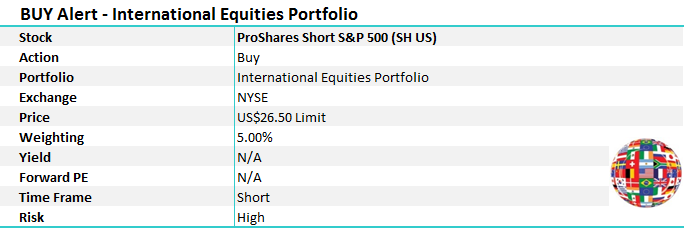

**We are adding the short US S&P 500 ETF to the International Equities Portfolio**

Major Movers Today – Netflix reported after the close in the US overnight and the report was weak. Expect the stock to be lower on open, down around 10%. Weakness over here is a buying opportunity.

Have a great night

James, Harry the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 18/07/2019

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report not withstanding any error or omission including negligence.