How could a change of Government and franking credit treatment impact Listed Investment Companies (LIC’s)

Listed Investment Companies (LIC) are a popular home for income conscious investors however as the Federal Election looms in a few months, its right to ask the question – will this sector be adversely impacted by the proposed change to franking credits?

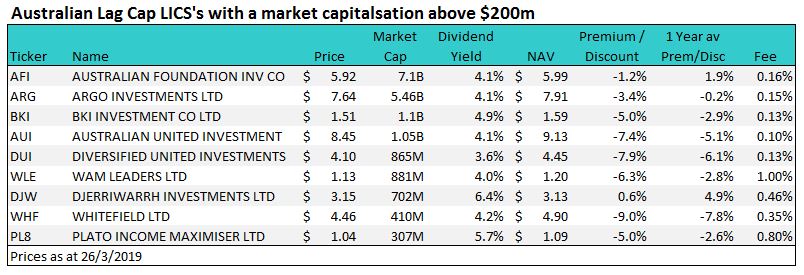

To recap, under a Labor Government which is likely in May, they plan to remove cash refunds for excess imputation credits – or in other words, those in a no / very low tax environment who get a cash refund from the ATO will no longer get it unless you’re a government supported pensioner, a charity or can take advantage of a few other carve outs. In general terms (and we stress general) a SMSF investor with a balance of $200,000 to $1 million will lose income, and all things being equal some LICs may become less attractive for this cohort. In today’s note, we’ll look at the larger LICs listed on the ASX, with most (but not all) offering attractive yields.

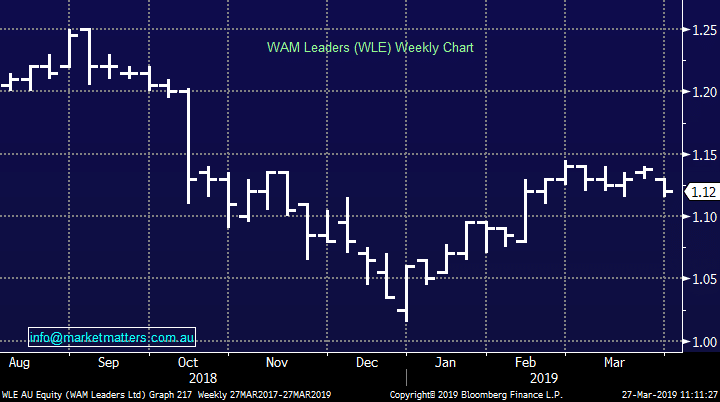

The list above covers LICs that invest in large cap Australian shares - a number of these have been around since Adam stumbled across Eve while some are more recent, the Plato Income Maximiser for instance listed in 2017 as the first LIC to pay monthly dividends. The majority of these trade at a discount to the value of their assets while some are at a slight premium. WAM Leaders (WLE) is the most expensive in terms of fees and trades at the biggest premium to the underlying value of its holdings while Australian United (AUI) is the cheapest in terms of fees.

WAM Leaders (WLE) Chart

The list above covers LICs that invest in large cap Australian shares - a number of these have been around since Adam stumbled across Eve while some are more recent, the Plato Income Maximiser for instance listed in 2017 as the first LIC to pay monthly dividends. The majority of these trade at a discount to the value of their assets while some are at a slight premium. WAM Leaders (WLE) is the most expensive in terms of fees and trades at the biggest premium to the underlying value of its holdings while Australian United (AUI) is the cheapest in terms of fees.

WAM Leaders (WLE) Chart

Whitefield (WHF) is the LIC in the above list offering most value relative to its assets, trading at a 9% discount, however they have underperformed their benchmark over 1,3,5 & 10 years, albeit by a small margin. Whether or not a LIC trades at a premium or discount happens for a few reasons, performance over time is key however communication with investors and potential investors is also very important. I had lunch yesterday with a good client of mine and about 10 years ago he put 500k into WAM , and got a call from Geoff Wilson welcoming him as a shareholder. That’s the sort of investor engagement that will drive a premium.

That said, we struggle with the concept of paying $1.25 for $1.20 worth of value and I would think Geoff Wilson may also grapple with that concept. On the contrary, he often uses his overvalued stock to buy into other LICs that are trading at a discount to their assets, which makes total sense, particularly if he can buy enough of them and eventually take over the management.

The table below shows WAM Capital (WAM) which is trading at a 21.6% premium to its assets meaning that a buyer is prepared to pay $2.25 for a company that holds assets worth $1.85. By doing that, you’re essentially backing management to extract more from that asset base over time which can be true for a company delivering a product or service, however in the case of an LIC it implies the stock market is extremely inefficient and WAM’s portfolio managers have an incredibly valuable edge.

Whitefield (WHF) is the LIC in the above list offering most value relative to its assets, trading at a 9% discount, however they have underperformed their benchmark over 1,3,5 & 10 years, albeit by a small margin. Whether or not a LIC trades at a premium or discount happens for a few reasons, performance over time is key however communication with investors and potential investors is also very important. I had lunch yesterday with a good client of mine and about 10 years ago he put 500k into WAM , and got a call from Geoff Wilson welcoming him as a shareholder. That’s the sort of investor engagement that will drive a premium.

That said, we struggle with the concept of paying $1.25 for $1.20 worth of value and I would think Geoff Wilson may also grapple with that concept. On the contrary, he often uses his overvalued stock to buy into other LICs that are trading at a discount to their assets, which makes total sense, particularly if he can buy enough of them and eventually take over the management.

The table below shows WAM Capital (WAM) which is trading at a 21.6% premium to its assets meaning that a buyer is prepared to pay $2.25 for a company that holds assets worth $1.85. By doing that, you’re essentially backing management to extract more from that asset base over time which can be true for a company delivering a product or service, however in the case of an LIC it implies the stock market is extremely inefficient and WAM’s portfolio managers have an incredibly valuable edge.

Calton Investments (CIN) above is at the other end of the spectrum, trading at such a large discount implies that the market has little faith in their stock picking abilities. While they had strong performance in earlier years, the last 3 have been tough, largely because their biggest holding – Event Hospitality (EVT) has traded down during the period. Interestingly, they have a massive 50% or $412m of the LIC in that stock which is the old Amalgamated Holdings for those with a good memory.

Along with another fund manager, Enbeear Pty Ltd, they own around 40% of EVT, while Enbeear also holds a large stake in CIN. All somewhat complex however it does go to show that understanding the underlying holdings of an LIC is very important, and looking beyond just discount / premium to assets and long term track record is critical. That’s really the key in determining whether or not an LIC will be impacted by the proposed change. If holdings are dominated by stocks that could be impacted, those with high fully franked yields and no growth, then the LIC may lose some of its appeal.

As LICs get bigger, performance tends to come back to the market and with that any premium should also come out.

Calton Investments (CIN) above is at the other end of the spectrum, trading at such a large discount implies that the market has little faith in their stock picking abilities. While they had strong performance in earlier years, the last 3 have been tough, largely because their biggest holding – Event Hospitality (EVT) has traded down during the period. Interestingly, they have a massive 50% or $412m of the LIC in that stock which is the old Amalgamated Holdings for those with a good memory.

Along with another fund manager, Enbeear Pty Ltd, they own around 40% of EVT, while Enbeear also holds a large stake in CIN. All somewhat complex however it does go to show that understanding the underlying holdings of an LIC is very important, and looking beyond just discount / premium to assets and long term track record is critical. That’s really the key in determining whether or not an LIC will be impacted by the proposed change. If holdings are dominated by stocks that could be impacted, those with high fully franked yields and no growth, then the LIC may lose some of its appeal.

As LICs get bigger, performance tends to come back to the market and with that any premium should also come out.

Of the high yielding LICs above, Perpetuals PIC has 36% of the fund in CBA (11.2%), WBC (8.3%), SUN (6.6%), WOW (5.5%) & TLS (4.5%) – a fairly vanilla sort of approach and it is trading at a 5% discount, so it’s probably okay.

Cadence (CDM) is slightly different with the ability to trade on the long and short side of the market – here and overseas, however like the recent debacle from L1 Capital (LSF), long/short funds have struggled, and the record from CDM has been particularly poor. Purely from a share price perspective, over the past 5 years Cadence has underperformed the ASX 300 by 45%, losing 1.99% versus the market which as gained 43%.

Cadence Capital (CDM) Chart

Of the high yielding LICs above, Perpetuals PIC has 36% of the fund in CBA (11.2%), WBC (8.3%), SUN (6.6%), WOW (5.5%) & TLS (4.5%) – a fairly vanilla sort of approach and it is trading at a 5% discount, so it’s probably okay.

Cadence (CDM) is slightly different with the ability to trade on the long and short side of the market – here and overseas, however like the recent debacle from L1 Capital (LSF), long/short funds have struggled, and the record from CDM has been particularly poor. Purely from a share price perspective, over the past 5 years Cadence has underperformed the ASX 300 by 45%, losing 1.99% versus the market which as gained 43%.

Cadence Capital (CDM) Chart

Platinum Capital (PMC) is actually more a growth manager with exposure in Australia and overseas however in reality, most exposure is in Asia with China (17%), Japan (16%) and Sth Korea (6.5%), along with US exposure at 17%. Their biggest holdings are Ping An Insurance, Samsung, Glencore and Alphabet, meaning that they are growth focussed, so how do they pay a 6.3% fully franked yield when investing in growth?

A LIC has the advantage of being able retain earnings, pay tax on those earnings and essentially build up a dividend reserve and a franking balance. This helps them to maintain a smooth and sustainable dividend over the long term (this is different to the newer sort of listed trust structures which are required to distribute all earnings to the underlying unit holders). They also hold shares that pay fully franked dividends which is another source of franking credits that can be passed onto shareholders.

Some LIC’s will eat into capital to maintain a dividend and they can also buy specific shares for income / franking reasons – companies paying big fully franked special dividends for instance can be appealing. This is all okay as long as performance stacks up, or, if performance is weak for a period, it’s only a short period. Where LICs (as is the case with all companies) get into some trouble is by maintaining a dividend when earnings or income aren’t covering it. This is more prevalent than you might think.

A number of high profile LIC managers have been very vocal against the change in franking credit policy – and rightly so, as Charlie Munger once said, “show me the incentive and I’ll show you the outcome”. That’s a cynical comment and a LIC manager should act in the interests of their shareholders – ultimately they work for them, and a lot of shareholders will be negatively impacted by this change which justifies the fierce opposition.

At Market Matters we think the LICs that are trading at a large premium to their asset values are most at risk from this proposed change if indeed it happens, while LICs that have some global exposure should be more immune.

Platinum Capital (PMC) is actually more a growth manager with exposure in Australia and overseas however in reality, most exposure is in Asia with China (17%), Japan (16%) and Sth Korea (6.5%), along with US exposure at 17%. Their biggest holdings are Ping An Insurance, Samsung, Glencore and Alphabet, meaning that they are growth focussed, so how do they pay a 6.3% fully franked yield when investing in growth?

A LIC has the advantage of being able retain earnings, pay tax on those earnings and essentially build up a dividend reserve and a franking balance. This helps them to maintain a smooth and sustainable dividend over the long term (this is different to the newer sort of listed trust structures which are required to distribute all earnings to the underlying unit holders). They also hold shares that pay fully franked dividends which is another source of franking credits that can be passed onto shareholders.

Some LIC’s will eat into capital to maintain a dividend and they can also buy specific shares for income / franking reasons – companies paying big fully franked special dividends for instance can be appealing. This is all okay as long as performance stacks up, or, if performance is weak for a period, it’s only a short period. Where LICs (as is the case with all companies) get into some trouble is by maintaining a dividend when earnings or income aren’t covering it. This is more prevalent than you might think.

A number of high profile LIC managers have been very vocal against the change in franking credit policy – and rightly so, as Charlie Munger once said, “show me the incentive and I’ll show you the outcome”. That’s a cynical comment and a LIC manager should act in the interests of their shareholders – ultimately they work for them, and a lot of shareholders will be negatively impacted by this change which justifies the fierce opposition.

At Market Matters we think the LICs that are trading at a large premium to their asset values are most at risk from this proposed change if indeed it happens, while LICs that have some global exposure should be more immune.