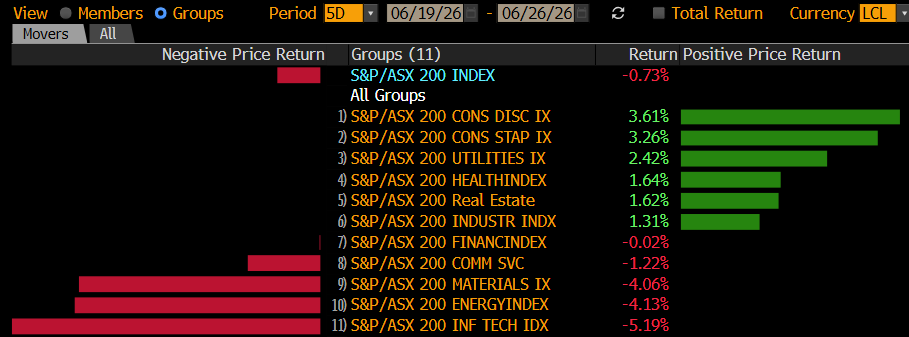

The ASX200 retreated by -0.7% on Thursday, yet the number of winners and losers was evenly matched. As we’ve touched on a few times this week, the market is going through a “risk-off” period with investors rotating into some of the more defensive and often underperforming names of FY26. If MM is correct and the $A finds support ~69c, the current aggressive profit-taking in the miners could be approaching its conclusion, perhaps in time for the start of FY27.

The ASX 200 rebounded 0.2% on Wednesday as ASX software names benefited from rotation out of Asian chipmakers, on what felt like a first for 2026, with gains the most aggressive where losses have been the steepest: WiseTech Global (+14%) and Xero (+9%). The toughest call at the moment is whether we are seeing some meaningful reversion, or simply ongoing EOFY book squaring.

The ASX200 lost early gains on Tuesday, as tech selling cascaded around the world following SpaceX’s ~16% fall in US trade. Yesterday's sell-off in the semiconductor stocks, some of the biggest beneficiaries of the AI boom, gathered momentum throughout the day, and saw the Korean Kospi close down 10%, with SK Hynix Inc. and Samsung Electronics Co. both sliding more than 12%.

The ASX 200 slipped 0.1% on Monday, not a bad performance considering US S&P 500 futures were trading lower, WiseTech (ASX: WTC) was hammered -18% following reports that police were investigating its chair, Richard White, and BHP Group (ASX: BH) fell another ~$1. Fortunately, the banks bucked the trend with all of the “Big Four” closing higher, a potential theme over the coming months, which we touched on in this week's Macro Monday Report.

The Fed may have left interest rates unchanged last week, but its accompanying commentary caught the market napping. Incoming Fed Chair Kevin Warsh's first FOMC meeting delivered a clear message: inflation remains the enemy, rate cuts are not guaranteed, and investors should continue to expect a data-dependent Fed.

The ASX200 ended its 4-day rally on Thursday, with 65% of the main board closing lower after the US Fed held interest rates in its first meeting under new Chair Kevin Warsh, but signalled that tightening may be necessary to rein in inflation. It was a relatively muted session for the local bourse with only five stocks moving by more than 5%, although they were all in the losers' corner, primarily from the gold space.

The ASX 200 enjoyed another solid performance on Wednesday, again reversing higher from early weakness to end the session up +0.6%, at a 2-month high and only a few points below the psychological 9000 level. It was a clear “risk on” session with only the defensive-oriented consumer staples and utilities sectors closing lower, along with the energy sector, which was weighed down by crude's inability to recover any of its recent ~15% drop over the last five days. From a points perspective, it was the heavyweight financials and miners that performed the heavy lifting, a very encouraging combination for the bulls.

The ASX shook off a weak start to finish firmly higher today, extending its recent recovery as investors continued rotating out of energy and into resources, financials and growth exposures. The market opened lower before steadily improving through the session, with buying increasing into the afternoon as optimism around US-Iran agreements accelerated with a proper framework and further details of the deal expected imminently.

The Reserve Bank of Australia (RBA), as expected, left interest rates at 4.35%, although Michelle Bullock warned that inflation remains too high. The central bank now faces a delicate balancing act, weighing stubbornly high inflation against mounting signs of softness across the labour market, consumer spending and housing sectors.

The ASX 200 rallied another +1.3% on Monday, following reports that the US and Iran have agreed on the terms of a peace deal. The index extended its advance for June to more than +2%, taking it back within ~3% of its February all-time high, ironically just before the US-Iran conflict erupted. Gains were fairly broad-based, with 70% of the main board advancing.

The ASX 200 rebounded 0.2% on Wednesday as ASX software names benefited from rotation out of Asian chipmakers, on what felt like a first for 2026, with gains the most aggressive where losses have been the steepest: WiseTech Global (+14%) and Xero (+9%). The toughest call at the moment is whether we are seeing some meaningful reversion, or simply ongoing EOFY book squaring.

The ASX200 lost early gains on Tuesday, as tech selling cascaded around the world following SpaceX’s ~16% fall in US trade. Yesterday's sell-off in the semiconductor stocks, some of the biggest beneficiaries of the AI boom, gathered momentum throughout the day, and saw the Korean Kospi close down 10%, with SK Hynix Inc. and Samsung Electronics Co. both sliding more than 12%.

The ASX 200 slipped 0.1% on Monday, not a bad performance considering US S&P 500 futures were trading lower, WiseTech (ASX: WTC) was hammered -18% following reports that police were investigating its chair, Richard White, and BHP Group (ASX: BH) fell another ~$1. Fortunately, the banks bucked the trend with all of the “Big Four” closing higher, a potential theme over the coming months, which we touched on in this week's Macro Monday Report.

The Fed may have left interest rates unchanged last week, but its accompanying commentary caught the market napping. Incoming Fed Chair Kevin Warsh's first FOMC meeting delivered a clear message: inflation remains the enemy, rate cuts are not guaranteed, and investors should continue to expect a data-dependent Fed.

The ASX200 ended its 4-day rally on Thursday, with 65% of the main board closing lower after the US Fed held interest rates in its first meeting under new Chair Kevin Warsh, but signalled that tightening may be necessary to rein in inflation. It was a relatively muted session for the local bourse with only five stocks moving by more than 5%, although they were all in the losers' corner, primarily from the gold space.

The ASX 200 enjoyed another solid performance on Wednesday, again reversing higher from early weakness to end the session up +0.6%, at a 2-month high and only a few points below the psychological 9000 level. It was a clear “risk on” session with only the defensive-oriented consumer staples and utilities sectors closing lower, along with the energy sector, which was weighed down by crude's inability to recover any of its recent ~15% drop over the last five days. From a points perspective, it was the heavyweight financials and miners that performed the heavy lifting, a very encouraging combination for the bulls.

The ASX shook off a weak start to finish firmly higher today, extending its recent recovery as investors continued rotating out of energy and into resources, financials and growth exposures. The market opened lower before steadily improving through the session, with buying increasing into the afternoon as optimism around US-Iran agreements accelerated with a proper framework and further details of the deal expected imminently.

The Reserve Bank of Australia (RBA), as expected, left interest rates at 4.35%, although Michelle Bullock warned that inflation remains too high. The central bank now faces a delicate balancing act, weighing stubbornly high inflation against mounting signs of softness across the labour market, consumer spending and housing sectors.

The ASX 200 rallied another +1.3% on Monday, following reports that the US and Iran have agreed on the terms of a peace deal. The index extended its advance for June to more than +2%, taking it back within ~3% of its February all-time high, ironically just before the US-Iran conflict erupted. Gains were fairly broad-based, with 70% of the main board advancing.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.