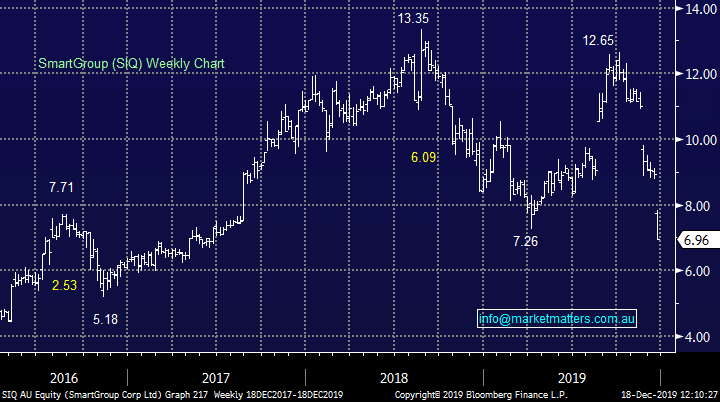

SmartGroup (SIQ) – trap or treasure?

Salary packaging business SmartGroup (SIQ) has declined from an October high of $12.65 to settle yesterday at ~$7, a painful ~44% decline thanks to a number of issues, however as we often say, the elastic band often stretches too far in both directions. Today, SIQ trades on a Est P/E for FY20 of 11.3x while it is expected to yield ~6.25% fully franked, Morgan’s the no 1rated analyst on the stock with an $8.57 price target. There have been three key issues for SIQ in the last couple of months that need consideration:

- Their largest shareholder Smart Packages sold their entire stake (~32m shares) in October via a block trade with Macquarie at $11.30. The stock was trading at $12.10 at the time, so the trade was done at a 6.6% discount to market. It was a $366m line of shares which is big, Macquarie took ~26m shares as principle (underwritten deal) and then sold them on. Smart Packages had crept up the register over time to get to ~25%, they were long term shareholders and used the rationale that the sale was a selfless one, simply to improve the liquidity of the SIQ register – I’m not so sure! Clients of Macquarie who took SIQ assuming $11.30 price tag are now ~40% underwater.

- About a month later, their long standing CEO Deven Billimoria announced his retirement to be succeeded by the long standing CFO, Tim Looi with SIQ now looking for a new CFO. That in itself if okay however Deven holds 3.3m shares / $23m and he’s now a natural seller of at least some of that by the look. The timing here is also questionable. Smart Packages supported SIQ from the early days before they listed, held through the initial ASX listing at $1.60 per share and a month after they sell their stake, the long standing CEO resigns! Again, some scepticism here required

- And finally, their latest update related to their insurance coverage after their underwriter confirmed intentions to change their product terms, a move that will cost them $4m from their FY20 net profits. If that number is annualised that equates to a ~10% earnings downgrade based on the company’s guidance for full year earnings of $81m.