Looking for value in the “drifting” insurance sector (SUN, QBE, IAG, NHF)

The ASX200 limped into the close yesterday closing down less than -0.1%, pretty much as we expected the markets slowly going quiet ahead of the next piece / phase of meaningful market news – this was always unlikely to unfold early this week with the US & UK closed last night for long weekends. On the sector level the financials were a touch softer while the resources found some buying led by the iron ore space which again enjoyed strong gains from Fortescue Metals (FMG), RIO Tinto (RIO) and the BHP Group (BHP) as Iron Ore Futures rallied during our time zone.

We saw another bid received by an Aussie company from an overseas player, this time Swedish company EQT aiming its sights on struggling Telco Vocus (VOC) – prior to the bid VOC was down almost 60% over the last 3-years while the $A was also down ~10% increasing the attraction to an overseas suitor. Interestingly the stock closed ~15% below the bid yesterday showing the perceived risks early on in these negotiations, we have no position but this feels like a ”Get out of jail free card” to long term holders of VOC if the bid firm up and the price edges towards the $5.25 price tag.

Two other things crossed my mind while I was considering this play by EQT and takeovers in general:

1 – Interest rates continue to fall to their lowest levels in history hence MM feels takeover activity looks set to reach a crescendo over 2019 /2020.

2 – The $A continues to struggle around decade lows enhancing the attraction of Australian companies to overseas players e.g. Vocus yesterday.

MM remains bullish the ASX200 technically while the index can hold above the 6350

Overnight US stocks were closed for Memorial Day with SPI futures pointing to an unchanged opening this morning.

In today’s report we are going to look at the Insurance sector which has noticeably struggled over the last week.

ASX200 Chart

A great example that bond yields, plus their respective interest rate differentials, are dominating markets at present is illustrated below when we consider the Aussie ($A) against the iron ore price.

Usually the $A tracks the iron ore price almost step for step but while Australian interest rates continue to fall below those in the US the market, and that’s clearly the main game on investor minds at the moment. i.e. interest rates remain the focus of today’s markets on a number of levels.

MM remains bullish the $A medium term but there are no signs of a reversal yet.

Australian Dollar ($A) v Iron Ore Chart

Australian 10-year bond yields v US 10-year bond yields Chart

Could the Insurance stocks decouple from the ASX200?

The markets enjoyed an excellent post-election rally but the performance by the Insurance sector has been far more mixed with the health insurers soaring while heavyweight’s QBE Insurance (QBE) and Suncorp (SUN) have struggled. We ask the question “is the sector which is usually so closely correlated to the ASX200 about to run its own course, plus more importantly are there any stocks within the sector where MM should be invested”.

At this stage the Insurance sector has only come back to the ASX200 after outperforming since later April.

ASX200 v Insurance sector Chart

1 Suncorp (SUN) $13.60

Suncorp (SUN) has endured a fairly tough 12-months falling ~15% while the ASX200 has made fresh decade highs, not a particularly exciting scorecard. Their last set of half yearly result showed weakness in their banking division which is hurting under growing competitive pressures while their insurance business was starting to improve on an underlying basis, however the financial markets and the cost of the storms turned an improving performance into a worse reported insurance profit.

1 – As interest rates fall SUN receives lower returns on the premiums it holds in cash to cover future claims while volatile markets have hindered the businesses ability to garner decent returns in other ways.

2 – The banking / insurance company has been hit over recent times with huge regulatory costs while natural disasters and hence claims have simply been occurring too often.

The stock is trading on a Est P/E for 2019 of 17x while it yields 5.8% fully franked, not too exciting compared to say Westpac which yields 6.7% fully franked while trading on a comparative P/E of 13.5x. Also technically SUN has been our “golden child” chart over the last 5-years and if this continues its destined to fall another ~20%.

Lastly, yesterday we saw the surprise departure of its CEO after 7 years on the board and 4-years in the top job, although according to the company’s release the business is operating as expected and should meet guidance. Also at play is the potential spin out of their banking division into a separate listed vehicle which would then allow Suncorp, as an insurance company to trade on a higher multiple without the drag of a subscale regional banking business. Perhaps this is the reason for the shock departure of the CEO.

MM is neutral SUN at best.

Suncorp (SUN) Chart

2 QBE Insurance (QBE) $12.32

QBE Insurance has had a simply awful 15-years which has seen problems throughout the business leading to the share price falling by over 60%. However, the fate of the insurer has improved over recent times as they have successfully simplified the business, improved their provisioning plus of course the tailwind of a strong $US has helped. The offset to these positive trends has been falling bond yields which has led to lower returns on invested funds.

The stock enjoyed 2019 rallying nicely allowing MM to take a healthy 20% profit on our holding back in March, a touch early but still at slightly higher levels than today. There is room for QBE to become a decent turnaround story and even though the stock continues to trade in a range, recent operational updates have either met or beat market expectations – slowly but surely QBE seems to be rebuilding credibility.

At today’s level the risk / reward is not compelling with the stock trading on an Est P/E for 2019 of 13.6x while yielding 4.1% part-franked.

MM is currently neutral QBE looking for weakness to buy.

QBE Insurance (QBE) Chart

3 IAG Insurance Australia (IAG) $7.89

IAG in similar fashion to SUN saw its cash earnings fall for the last 6-months of 2018 courtesy of last Decembers huge hail storms in Sydney. Also, this time like QBE they are trying to consolidate their business, in IAG’s case by attempting to sell off large parts of its South Asian operations.

One of the attractive parts of IAG is that it has plenty of capital and that could drive some capital management at their next result, however the run up in share price in recent months now the leaves IAG on the expensive side of the ledger.

Technically IAG is neutral while the numbers have a similar feel with the stock currently set to yield around 4.4% fully franked this year while trading on an Est P/E of 21.5x.

MM is currently neutral IAG.

Insurance Australia Group (IAG) Chart

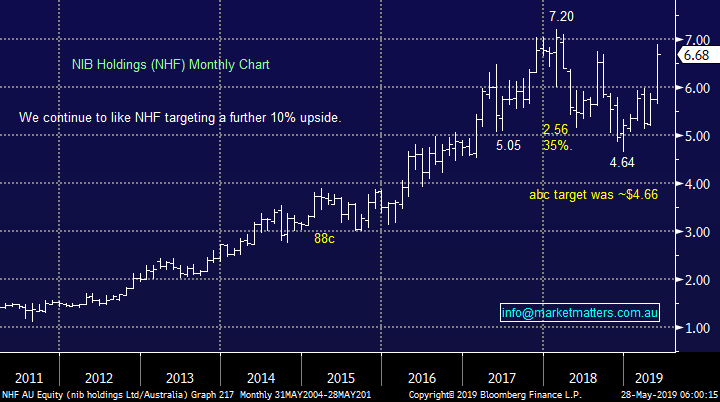

4 NIB Holdings (NHF) $6.68

We have discussed NIB Holdings (NHF) a number of times since the Federal election and happily for our Growth Portfolio position NHF has held onto its recent strong gains, technically it looks poised to make fresh highs above its early 2018 $7.20 level.

The short-term outlook for private health insurers NIB and Medibank Private is clearly better under a Coalition government but for real upside to unfold we need to see a change in trend between claims growth and premium growth. Currently, industry data shows claims growth outpacing premium growth creating an obvious challenge for insurance profits.

Last week, we saw the CEO Mark Fitzgibbon had sold $532k of his shares on the 21st of this month however considering he still owns well over $10m in stock, this sale to meet apparent tax obligations, is not a major red flag for MM.

MM remains bullish NHF initially looking for 10% upside.

NIB Holdings (NHF) Chart

Conclusion (s)

MM has no interest in the Insurance sector at this stage with the exception of Private health operators – we own NHF in the MM Growth Portfolio.

We will likely revisit QBE into weakness, although that seems some way off.

SUN remains weak technically however any potential spin off of their banking division would be a positive.

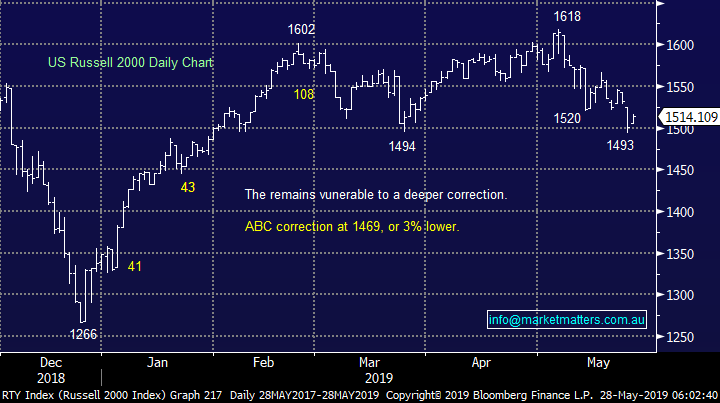

Global Indices

Nothing new with the US closed for Memorial Day.

US Russell 2000 (small cap) Index Chart

No change with European indices, we remain cautious European stocks but the tone is improving fast.

German DAX Chart

Overnight Market Matters Wrap

· A quiet session was experienced overnight, with both the US and UK closed for their respective public holidays.

· The Euro equity markets closed higher overnight after the EU elections, with the German DAX rallying 0.5%.

· The June SPI Futures is indicating the ASX 200 to open marginally higher, around the 6460 level this morning.

Have a great day!

James & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 28/05/2019

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report not withstanding any error or omission including negligence.