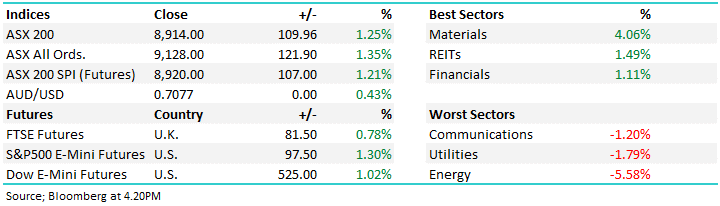

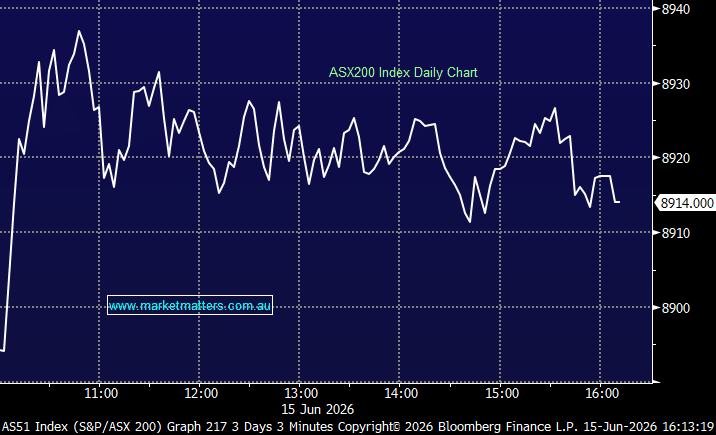

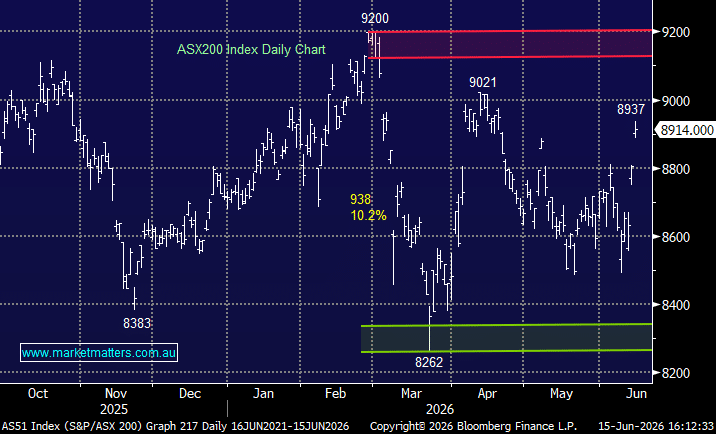

After a shaky start to the week, the ASX200 finished with a flourish, rallying 2% on Friday to end the week up 1.4% as risk appetite returned. Following several sessions dominated by geopolitical headlines, the ASX delivered its strongest weekly gain in two months as markets embraced the prospect of a US-Iran peace deal and the accompanying pullback in oil prices, which reversed more than US$10/barrel from their weekly highs.

The gains were driven primarily by rate-sensitive sectors, with Consumer Staples (+9%), Consumer Discretionary (+8%), Healthcare (+7%) and Real Estate (+5%) leading the charge.

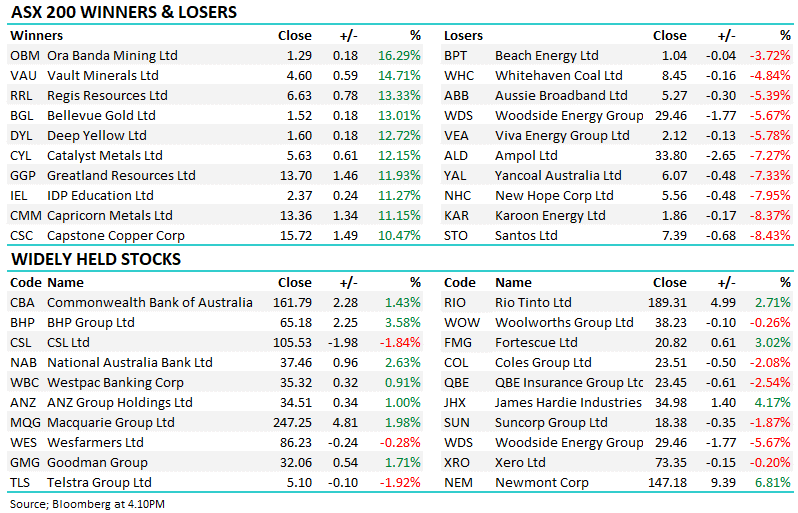

The winners' enclosure was also dominated by underperformers as investors went bargain hunting into EOFY, while the laggards had a distinctly gold and uranium flavour.

The ASX 200 fell 1.2% for the week as weakness in Financials (-2.1%) and Materials (-2.4%) offset a strong rebound in technology stocks. The ASX Tech Sector surged 7.7%, led by Pro Medicus (+25%), Megaport (+23%) and WiseTech Global (+11%), as investor concerns around AI disruption eased.

Market sentiment remained cautious amid escalating US-Iran tensions, falling iron ore prices and ongoing softness in the Australian property market. Miners, banks and gold stocks were among the worst performers, while investors increasingly rotated towards defensive sectors.

A stronger-than-expected US jobs report late in the week pushed bond yields higher and reignited concerns that the Federal Reserve may need to keep interest rates elevated. The NASDAQ fell 4.8%, its sharpest decline since April 2025.

Looking ahead, US CPI data will be the key focus. A softer inflation reading could support growth and technology stocks, while a stronger result may pressure rate-sensitive sectors and reinforce expectations of further policy tightening.

SPI Futures currently suggest the ASX 200 could open around 1.3% lower when trading resumes.

The ASX200 ended the week surging +1.6% higher on Friday, turning around the market's fortunes to end the week up +0.9%, and up +0.5% for May - a clear demonstration that investors need to look through the volatile noise emanating from the US-Iran War. It was another week of sharp daily swings as markets rode the emotional roller-coaster of the conflict. However, sentiment improved into Friday after reports emerged that the US and Iran had agreed to a tentative 60-day ceasefire extension to allow further negotiations over Tehran’s nuclear program, raising hopes the three-month conflict may finally be moving towards de-escalation.

The ASX200 needed a storming return to form on Thursday & Friday to end the week up just +0.3%, as news around the US-Iran War finally supported local stocks. The choppy week saw early negative sentiment push the index down to a fresh 7-week low, testing below the 8500 level before some bargain hunting returned. The major miners led the market's recovery, reflecting an improvement in risk appetite given the sector’s strong leverage to global growth expectations, although both BHP Group (ASX: BHP) and Rio Tinto (ASX: RIO) still finished the week modestly lower.

The ASX200 fell 1.3% last week, with market sentiment softened by Tuesday’s Budget and disappointing trading updates from ASX heavyweights CBA and CSL - as the saying goes, the trend’s your friend, with the previous market darling CSL, now down -43%, in 2026. As we all know, the budget played a dominant role last week, with the influential “Big Four Banks” retreating by an average of close to 6% on fears around Australia's pivotal housing market. It’s a good job the big miners enjoyed a great week, despite surrendering some of their gains on Friday. BHP Group (ASX: BHP) and RIO Tinto (ASX: RIO) posted fresh all-time highs, both advancing +4% by Friday's close.

The ASX200 experienced a choppy week, ultimately closing up +0.2% following Fridays triple-digit loss as tensions between the US and Iran took a turn for the worse. The local index was threatening to break out toward fresh highs on Thursday before yesterday’s -1.5% sell-off, leaving the market stuck in the 8600-9000 trading range where it’s now looked comfortable for more than a month. The rate-sensitive stocks continue to weigh on the ASX with retail and real estate continuing to drag the local index back despite the best efforts of the miners which saw the materials sector gain +4.3% through the week, with more set to come on Monday.

The ASX200 ended its 8-day losing streak on Friday with a solid +0.7% advance, although it promised more early on before the “Big Four Banks” reversed lower. It felt worse, but come the closing bell on Friday, the index was only down 0.6% for the week, although compared to the strong gains in the US, it was a clear disappointment. It was the big end of town that reined in the market last week, with the banks and heavyweight miners retreating. Next Wednesday, we see the RBA step up on interest rates, with credit markets pricing in a ~74% probability of a 0.25% hike, while on the following Tuesday, we will receive the Federal Budget- there’s no rest for the wicked in May!

The ASX200 ended the penultimate week of April, surrendering -1.8% of the month's gain, with a string of profit downgrades combining with the country’s high vulnerability to the global fuel crisis caused by the Iran war - the oil price continues to grind higher with no clear resolution in sight for the conflict. A wave of profit downgrades swept the ASX, led this week by Cochlear’s earnings shock, which sent its shares plunging 40%. Other companies warning that surging energy costs will weigh on earnings included Qantas, Worley, a2 Milk, Orora, Cleanaway and Qube. The ASX is also struggling because its two heavyweight sectors have come off the boil, the banks and resources.

The ASX200 finished the week down -0.2%, snapping a 3-week winning streak as it failed to embrace the strength across global indices. A +13% surge by the tech sector wasn't enough to offset losses by the influential banks, with the financial sector ending the week down -2.1%. Westpac set the tone early in the week, flagging that interest-rate volatility tied to the Iran conflict had hit its market’s income and prompted higher credit provisions. While not unexpected given rising rates, cost-of-living pressures and higher fuel prices, the update reinforced a cautious “if in doubt, get out” stance from investors ahead of May results from ANZ, NAB and Westpac

The ASX 200 fell 1.2% for the week as weakness in Financials (-2.1%) and Materials (-2.4%) offset a strong rebound in technology stocks. The ASX Tech Sector surged 7.7%, led by Pro Medicus (+25%), Megaport (+23%) and WiseTech Global (+11%), as investor concerns around AI disruption eased.

Market sentiment remained cautious amid escalating US-Iran tensions, falling iron ore prices and ongoing softness in the Australian property market. Miners, banks and gold stocks were among the worst performers, while investors increasingly rotated towards defensive sectors.

A stronger-than-expected US jobs report late in the week pushed bond yields higher and reignited concerns that the Federal Reserve may need to keep interest rates elevated. The NASDAQ fell 4.8%, its sharpest decline since April 2025.

Looking ahead, US CPI data will be the key focus. A softer inflation reading could support growth and technology stocks, while a stronger result may pressure rate-sensitive sectors and reinforce expectations of further policy tightening.

SPI Futures currently suggest the ASX 200 could open around 1.3% lower when trading resumes.

The ASX200 ended the week surging +1.6% higher on Friday, turning around the market's fortunes to end the week up +0.9%, and up +0.5% for May - a clear demonstration that investors need to look through the volatile noise emanating from the US-Iran War. It was another week of sharp daily swings as markets rode the emotional roller-coaster of the conflict. However, sentiment improved into Friday after reports emerged that the US and Iran had agreed to a tentative 60-day ceasefire extension to allow further negotiations over Tehran’s nuclear program, raising hopes the three-month conflict may finally be moving towards de-escalation.

The ASX200 needed a storming return to form on Thursday & Friday to end the week up just +0.3%, as news around the US-Iran War finally supported local stocks. The choppy week saw early negative sentiment push the index down to a fresh 7-week low, testing below the 8500 level before some bargain hunting returned. The major miners led the market's recovery, reflecting an improvement in risk appetite given the sector’s strong leverage to global growth expectations, although both BHP Group (ASX: BHP) and Rio Tinto (ASX: RIO) still finished the week modestly lower.

The ASX200 fell 1.3% last week, with market sentiment softened by Tuesday’s Budget and disappointing trading updates from ASX heavyweights CBA and CSL - as the saying goes, the trend’s your friend, with the previous market darling CSL, now down -43%, in 2026. As we all know, the budget played a dominant role last week, with the influential “Big Four Banks” retreating by an average of close to 6% on fears around Australia's pivotal housing market. It’s a good job the big miners enjoyed a great week, despite surrendering some of their gains on Friday. BHP Group (ASX: BHP) and RIO Tinto (ASX: RIO) posted fresh all-time highs, both advancing +4% by Friday's close.

The ASX200 experienced a choppy week, ultimately closing up +0.2% following Fridays triple-digit loss as tensions between the US and Iran took a turn for the worse. The local index was threatening to break out toward fresh highs on Thursday before yesterday’s -1.5% sell-off, leaving the market stuck in the 8600-9000 trading range where it’s now looked comfortable for more than a month. The rate-sensitive stocks continue to weigh on the ASX with retail and real estate continuing to drag the local index back despite the best efforts of the miners which saw the materials sector gain +4.3% through the week, with more set to come on Monday.

The ASX200 ended its 8-day losing streak on Friday with a solid +0.7% advance, although it promised more early on before the “Big Four Banks” reversed lower. It felt worse, but come the closing bell on Friday, the index was only down 0.6% for the week, although compared to the strong gains in the US, it was a clear disappointment. It was the big end of town that reined in the market last week, with the banks and heavyweight miners retreating. Next Wednesday, we see the RBA step up on interest rates, with credit markets pricing in a ~74% probability of a 0.25% hike, while on the following Tuesday, we will receive the Federal Budget- there’s no rest for the wicked in May!

The ASX200 ended the penultimate week of April, surrendering -1.8% of the month's gain, with a string of profit downgrades combining with the country’s high vulnerability to the global fuel crisis caused by the Iran war - the oil price continues to grind higher with no clear resolution in sight for the conflict. A wave of profit downgrades swept the ASX, led this week by Cochlear’s earnings shock, which sent its shares plunging 40%. Other companies warning that surging energy costs will weigh on earnings included Qantas, Worley, a2 Milk, Orora, Cleanaway and Qube. The ASX is also struggling because its two heavyweight sectors have come off the boil, the banks and resources.

The ASX200 finished the week down -0.2%, snapping a 3-week winning streak as it failed to embrace the strength across global indices. A +13% surge by the tech sector wasn't enough to offset losses by the influential banks, with the financial sector ending the week down -2.1%. Westpac set the tone early in the week, flagging that interest-rate volatility tied to the Iran conflict had hit its market’s income and prompted higher credit provisions. While not unexpected given rising rates, cost-of-living pressures and higher fuel prices, the update reinforced a cautious “if in doubt, get out” stance from investors ahead of May results from ANZ, NAB and Westpac

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.