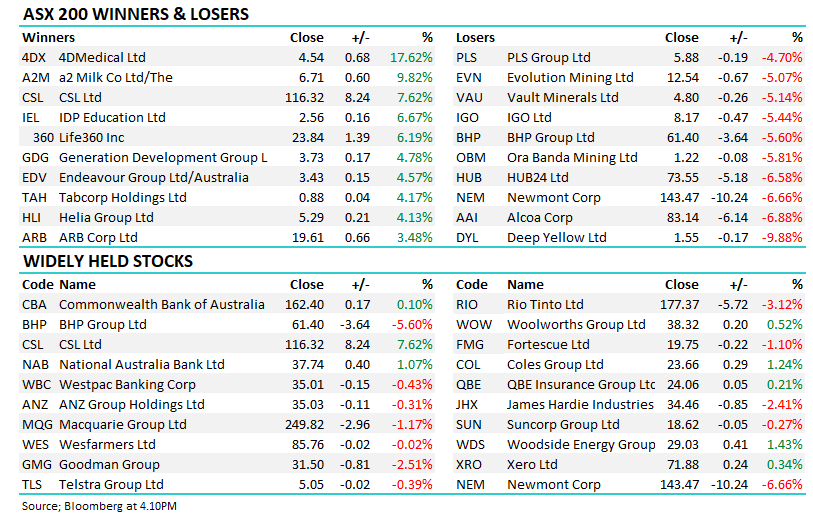

Sector rotation rules supreme

A huge day on the reporting front today along with news from Canberra that another tilt by Peter Dutton at the Liberal leadership is imminent. This is likely to underpin more volatility on a stock level throughout the day. Before we get into today’s report, two companies we hold in the Growth Portfolio reported yesterday. Click here for reporting calendar

A2 Milk (A2M) delivered a strong full year result yesterday with profit coming in above expectations by around ~3.5% along with strong underlying trends in terms of margins and guidance into FY19. A2 continues to deliver on growth, and execution of their strategies. They also announced a deal to distribute their products into Walmart stores across New York, Pennsylvania, Florida, Texas, Maryland and Washington, in what looks to be a pilot program in the US. Although this is unlikely to be meaningful to earnings for some time, it’s another avenue for future growth. The stock added +5.05% yesterday to close at $10.60.

Newcrest (NCM) reported after market yesterday and they beat expectations by a reasonable margin, although some of the beat was a result of an insurance payout. That said, it’s another incremental step in NCM under promising and over delivering on a consistent basis. On the numbers, NCM reported FY18 underlying NPAT $459.0m vs. expectations of around $400m.

The MM Growth Portfolio outperformed the ASX200 by 0.6% yesterday – which is nice but irrelevant over such a short period of time. While it was pleasing to see two of our holdings Telstra (TLS) and A2 Milk (A2M) see strong buying, it was hard not to have “stock envy” when considering the massive runs we saw in WiseTech (WTC) and Altium (ALU).

Looking at broker moves this morning on both of those, the market is still well behind the curve here even after upgrades yesterday. The most bullish broker on WTC is Morgan Stanley with a $17 PT v current stock price of $19.90 while on Altium (ALU), Bells are the most bullish with a $27.50 PT relative to yesterdays close of $28.75. These stocks are momentum plays and it seems some momentum funds pushed hard on them yesterday. It will be interesting today to see if the $110m capital raise announced by Afterpay (APT) this morning will rip some money out of the sector.

The local political fiasco rolls on but 3 things I believe sum up where things sit from a market perspective:

- When Labor win the next election (just check the bookies odds) stocks which have been in favour for years due to franking credits are likely to struggle.

- The housing market will also struggle under Labor as they intend to limit negative gearing.

- It feels irrelevant whether Dutton or Turnbull leads the Liberal Party into the next election, Labor look set to win.

However, at least one thing made me laugh on this subject yesterday, Julia Bishops scathing rebuff of Karl Stefanovic in an interview definitely worth checking out whatever your political bias. A thought from MM – buy local stocks, especially banks if Julia Bishop stands to lead the Liberals, this is the person who Labor fear the most in the polls.

· We are now neutral / negative the ASX200 after the close below 6300 while remaining in “sell mode” albeit still in a patient manner.

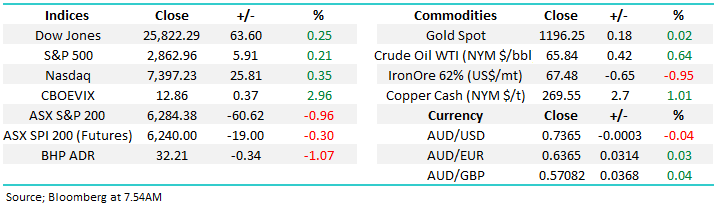

Overnight stocks were mixed but not as bad as the futures were implying during our time zone, the ASX200 is poised to open up around 15-points courtesy of the Oil Sector which rallied strongly in the US dragging BHP along for the ride, it closed up over 2% on the US ADR market.

Today’s report is going to take a breather from delving into the current volatile reporting season and switch back to one of our favourite subjects “sector rotation”.

The last few reports have touched on the merits of picking the times to be over / underweight equities but arguably the most value can be added to a portfolio by deciding which sectors to own at any period of time.

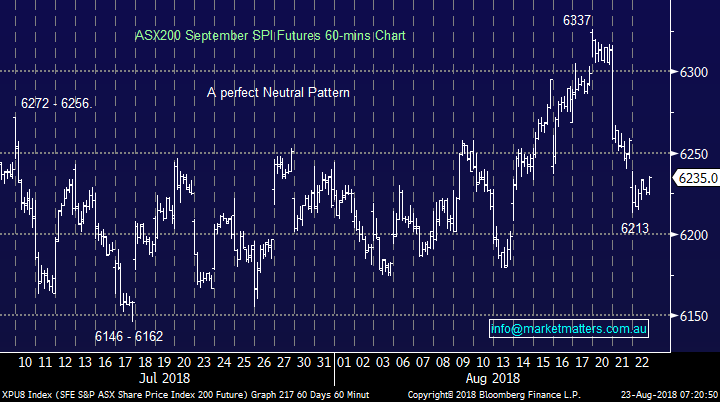

ASX200 Chart

As we’ve discussed a few times recently the best vehicle to identify a downturn in the Australian market at this time of year is the September futures (SPI) and maybe it’s time to pay attention.

· MM received a technical “sell signal” from the SPI following decent volume trading below 6250 on Tuesday

Our optimum first target is the 6150 area but following yesterday’s fall and partial recovery we expect a few days consolidation before any further leg (s) south.

ASX200 September SPI Futures Chart

Sector rotation

Today I have briefly looked at 6 major sectors within the ASX200 as we strive to add value / alpha to the MM portfolio’s. We may bore down into a few of these sectors over the coming weeks if / when opportunities feel close to hand.

The catalyst for this report was not surprisingly the Telco Sector which has now rallied over 25% during the last month while the Materials (Resources dominated) Sector has fallen ~3%, however a month ago nobody wanted to talk Telco’s and they were mostly in love with the resources i.e. our optimism / pessimism elastic band analogy was simply stretched too far.

1 The Bank Sector

The Australian Banking Sector has come back into vogue slightly over recent months but it remains a huge underperformer since the ASX200 which has rallied 35% from its 2016 low.

While the current political turmoil and very real threat of a Labor victory in the next election is a clear negative to our Banking Sector we feel further aggressive selling will provide another buying opportunity.

· MM believes the Banking Sector will outperform the ASX200 over the next 12-18 months i.e. play some relative catch-up.

The ASX200 v The Banking Sector Chart

2 The Telco Sectors

The Australian Telecom Sector surged over 14% yesterday as a potential merger of TPG Telecom and Vodafone allayed the markets concerns of an ongoing mobile price war i.e. increased margins for the sector moving forward.

A follow on from this would be the potential for Telstra (TLS) to pay a higher dividend than forecast by most analysts – on the news TLS rallied +7.2% and TPG Telecom (TPM) +27% to produce a simply amazing sector performance.

· MM continues to believe that the Telco Sector will be an outperformer in 2018/9 – we remain happy with our TLS exposure.

The ASX200 v The Telco Sector Chart

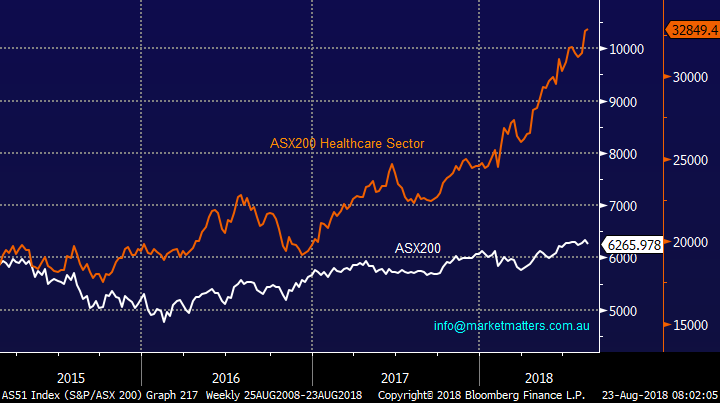

3 The Healthcare Sector

The Australian Healthcare Sector has performed admirably since the market bottomed in 2016 but the “ageing population” is now a well-trodden investment thematic and we believe investors have become too complacent in this area – remember former market favourite Ramsay Healthcare (RHC) has now corrected well over 30% over the last few years.

Undoubtedly the sector contains some of our best companies with excellent exposure to offshore earnings but they are being almost priced for perfection. We prefer to be buyers of corrections as opposed to chase strength in the sector.

· MM believes the Healthcare Sector will now trade in-line with the ASX200 and are interested in buying retracements, not chasing strength.

NB We have practiced what we are preaching above having recently bought Healthscope and Ramsay Healthcare (RHC) into weakness.

The ASX200 v The Healthcare Sector Chart

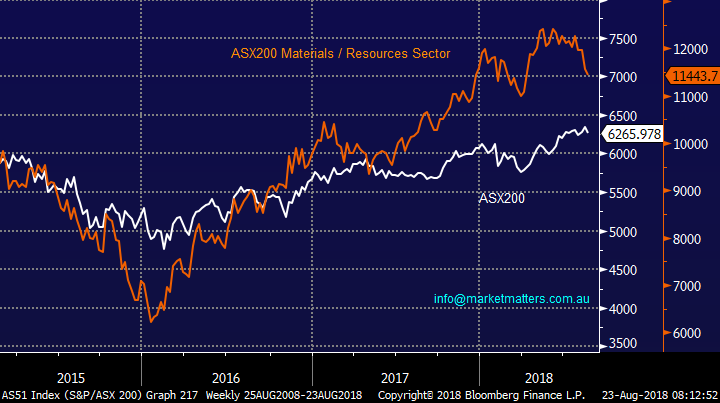

4 Resources

The Australian Resources Sector has enjoyed a stellar run since early 2016 but we believe the easy money is well and truly gone with a number of stocks recently correcting e.g. RIO Tinto (RIO) -18%, OZ Minerals (OZL) -20% and Western Areas (WSA) -33%. One of the reasons the MM portfolios have outperformed recently has been our lack of exposure to resources.

We jumped off the resources band wagon a touch early in most cases but at least we enjoyed some nice profits and the stocks are now mostly well below our exit levels, the question is what now.

MM is looking to re-enter the sector around 4-5% lower in anticipation of another decent advance , remember as inflation increases the resources sector should outperform.

· MM is looking to re-enter the resources sector around 4-5% lower.

The ASX200 v The Resources Sector Chart

5 Retail Sector

The Australian Retail Sector has improved recently mainly because pessimism had become way too entrenched leaving plenty of room for a “pop higher”.

MM had some technical buy signals in stocks like Harvey Norman (HVN) but due to the fundamental picture we have not embraced the sector (aside from Nick Scali (NCK) in the income portfolio) i.e. Australian household debt remains a major concern to us.

· MM is neutral the Retail Sector at present however it’s clear by the recent move that the sector is under owned.

The ASX200 v The Retail Sector Chart

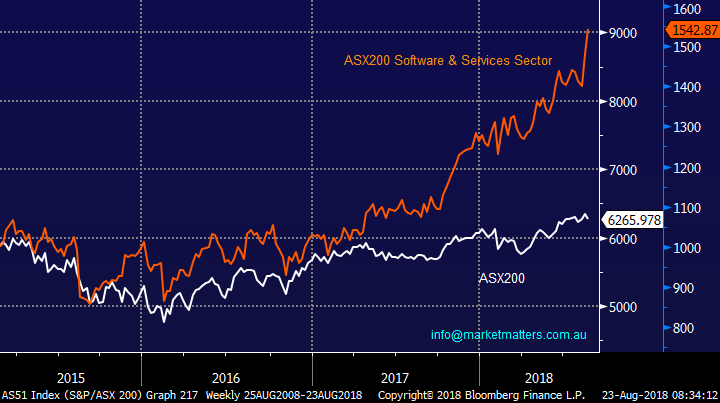

6 Software & Services

The Software & Services Sector has exploded since 2017 rallying 39% over the last year led by the likes of Xero (XRO), REA Group (REA) and Computershare(CPU).

Time for our “big call” today, we believe the risk / reward from these extremely high valuation / growth stocks is poor and we are now outright negative.

· MM believes the Software & Services Sector is due for a period of underperformance – todays cap raise from APT has perhaps rung the bell on the sector!

The ASX200 v The Software & Services Sector Chart

Conclusion

Of the 6 sector we covered we have mixed views over different timeframes but a quick summary is:

1 Banks should outperform during 2018/9 albeit with some volatility courtesy of our politicians.

2 Telco’s should outperform during 2018/9.

3 The Healthcare sector now only looks a buy into weakness.

4 The resources will look attractive ~4-5% lower for a relatively short-term position.

5 We are neutral the Retail Sector having differing signals from the technical and fundamental pictures.

6 We believe the Software & Services Sector is due for a period of underperformance.

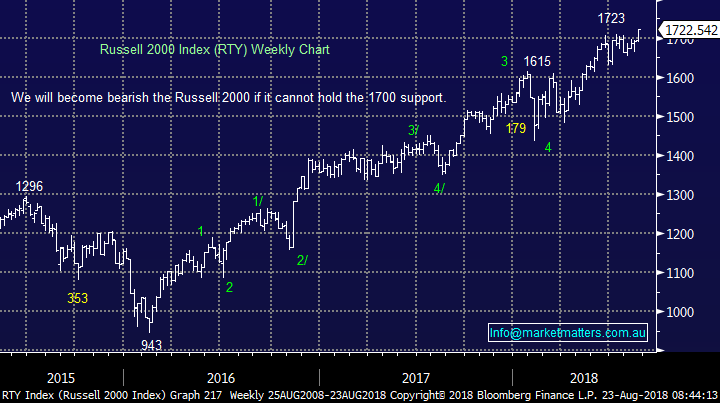

Overseas Indices

The indices continue to hover around all-time highs, we are watching the Russell 2000 closely, a close below 1700 will generate a technical sell signal for us.

US Russell 2000 Index Chart

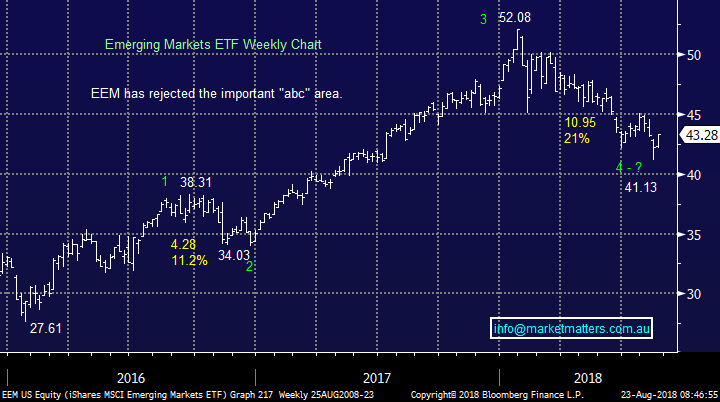

As is so often the case markets panic and then things blow over, we ponder if this will again be the case for the emerging markets as I haven’t heard Turkeys name for a few days.

Emerging Markets ETF Chart

Overnight Market Matters Wrap

· Another quiet session in the US overnight, as investors digest the Fed Reserve minutes that indicates the maintenance of a gradual pace of rate hikes, while most ignored the criminal convictions of Trumps former lawyer Michael Cohen and his campaign manager Paul Manafort.

· Domestically, the following companies are expected to report their earnings – AWC, APO, FLT, IRE, NEC, NST, PTM, QAN, QUB, STO, S32, SGP, SXL, VVR, WEB.

· The September SPI Futures is indicating the ASX 200 to open 20 points higher towards the 6285 level this morning.

Have a great day!

James & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 23/08/2018

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.

To unsubscribe. Click Here