Should we be jumping on board the iron ore train?

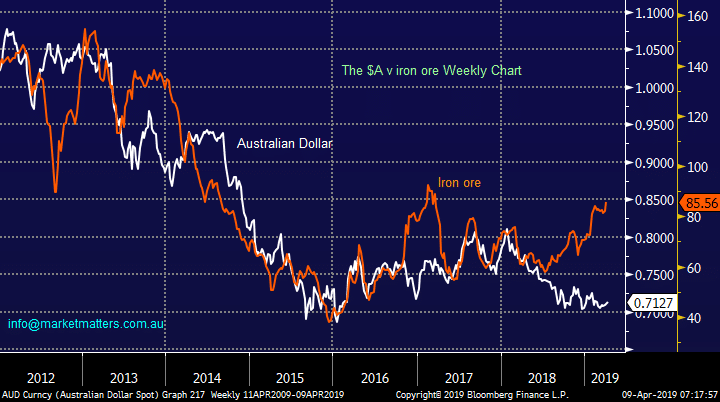

We have shown the below chart a number of times over recent weeks and we continue to believe its an elastic band tightening by the day for iron ore and $A – we remain bullish the $A targeting a test of 80c.

Currently local resources are enjoying the perfect tailwind of rising underlying commodity prices while the $A remains very subdued. We believe part of this tailwind will be removed medium-term but if iron ore remains at current levels, or rises further, a stronger $A is unlikely to significantly harm the miners.

Conversely If we look at the chart below the last time the $A ignored a strong rally in iron ore was in late 2016 when the currency proved correct as the bulk commodity proceeded to tumble 30% - a scenario few are considering today.

$A v iron ore Chart

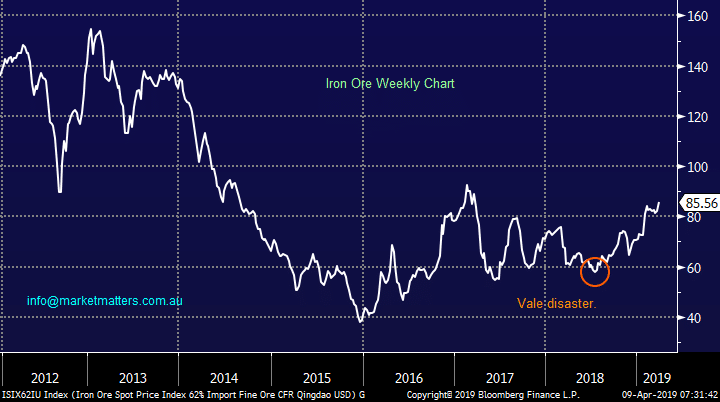

The iron ore chart (s) below shows the sharp rally in the bulk commodity since the Vale disaster this year on the 25th of January.

If we were looking at the first chart from a purely technical perspective we would now have a target well over $US100/tonne medium-term (in line with Citi’s view) although the picture is not as clear in the Chinese Renminbi futures contract.

However this is a market with many strong driving fundamental issues with the previously mentioned Vale supply the most important this year, sharp 10-20% pullbacks is almost common for the commodity and it could easily be far more if Vale were to just hint at returning some decent supply in the future.

Iron ore ($US/tonne) Chart

The iron ore chart (s) below shows the sharp rally in the bulk commodity since the Vale disaster this year on the 25th of January.

If we were looking at the first chart from a purely technical perspective we would now have a target well over $US100/tonne medium-term (in line with Citi’s view) although the picture is not as clear in the Chinese Renminbi futures contract.

However this is a market with many strong driving fundamental issues with the previously mentioned Vale supply the most important this year, sharp 10-20% pullbacks is almost common for the commodity and it could easily be far more if Vale were to just hint at returning some decent supply in the future.

Iron ore ($US/tonne) Chart

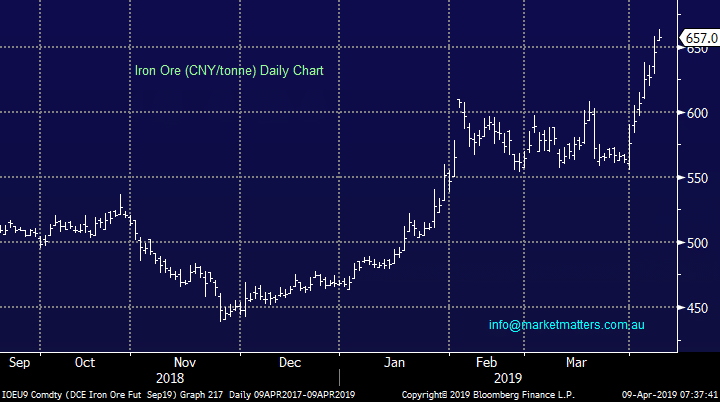

Iron ore Futures (CNY/tonne) - China Chart

Iron ore Futures (CNY/tonne) - China Chart

This post is a excerpt from Market Matters morning report from the 9th of April in which we spoke about our Iron Ore views as we well as specific views on a number of stocks. Subscribe to receive full reports

This post is a excerpt from Market Matters morning report from the 9th of April in which we spoke about our Iron Ore views as we well as specific views on a number of stocks. Subscribe to receive full reports