High Yield = High Risk… IOOF (IFL) a case in point

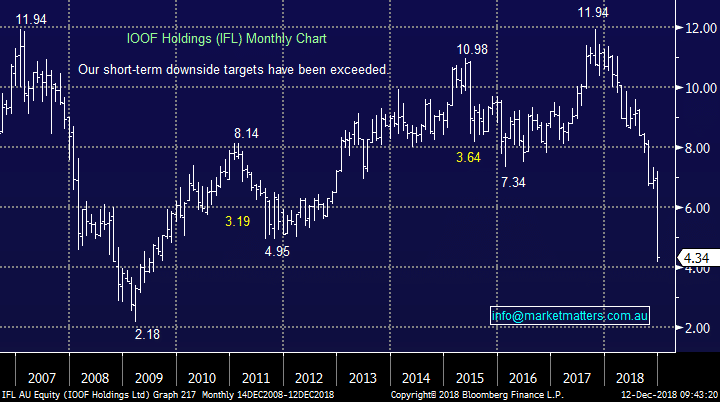

We’ve covered the woes of AMP a number of times in the MM Income note however questions consistently arise around whether or not it’s a ‘good yield play’ at the moment. It trades on a current P/E of 8.9x (cheap) and according to analyst consensus and while their dividend will be cut, they’ll still pay 24cps during 2019 putting it on a 10.57% yield plus franking, or a massive 15.1% gross. To recap, we penned the following article in July and although the share price has continued to slide, we still have no interest in the Financial Services stock (yet); Without stating the obvious, AMP faces some major challenges However, the more interesting case at the moment seems to be the woes facing IOOF (IFL), a stock that has traded from above $11 to close yesterday at $4.34. The wealth manager / platform provider trades on an expected P/E of just 6.9x while yielding 12.90% fully franked according to Bloomberg consensus, which adding franking equates to a massive 18.42% - clearly this must be an anomaly and the high yield simply implies the dividend will be cut – maybe not! As means of background, IOOF was already facing headwinds from the Royal Commission shortly after agreeing to buy the ANZ Wealth Business which as we now know was at the top of the market. We actually held IFL in the Growth Portfolio and took a loss on the position back in June saying at the time… While we believe IFL is cheap relative to its current earnings profile, we are cutting our position for a ~12% loss given the increasing complexity around future earnings on a number of fronts. Quite simply, we think there are too many variables for IFL at this point in time. Sell – take a loss and look elsewhere.

IOOF (ASX: IFL) Chart

In the last week or so we’ve now seen the MD Chris Kelaher and the Chairman George Venardos step down and are very unlikely to ‘step back up’ after APRA took action to impose licence conditions on IOOF’s APRA regulated entities while they are also seeking disqualification orders. This effectively means that the ANZ Wealth deal may fall over (net negative for ANZ & IFL) plus they’ll likely see a bigger uptick in outflows from their existing advice and platform businesses, while the big elephant in the room is the impact of reputational damage on the business. Just like AMP and every other Wealth Management business in the country, trust is at the epicentre of everything they do, reputational damage is very hard to repair (and quantify).

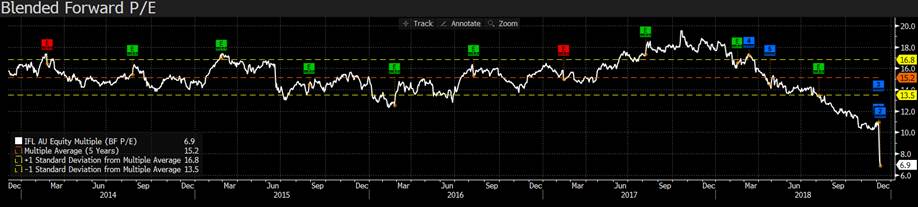

While the share price has taken a major hit and analysts have downgraded price targets aggressively, Citi for instance went from $8.65 to $4.50, Credit Suisse cut from $10.00 to $4.60 and Morgan Stanley from $10.80 to $5.00 - significant re-rates which shows how ‘wrong’ the market has been on this stock, digging into the downgrades, it’s more a function of increasing ‘risk premium’ being used than a big cut to earnings expectations. For example, consensus earnings per share before this latest news was around 67c however that number is now at 61c, a 10% downgrade at the earnings line but price targets as outlined above have been cut by around ~50%. Why?

In the last week or so we’ve now seen the MD Chris Kelaher and the Chairman George Venardos step down and are very unlikely to ‘step back up’ after APRA took action to impose licence conditions on IOOF’s APRA regulated entities while they are also seeking disqualification orders. This effectively means that the ANZ Wealth deal may fall over (net negative for ANZ & IFL) plus they’ll likely see a bigger uptick in outflows from their existing advice and platform businesses, while the big elephant in the room is the impact of reputational damage on the business. Just like AMP and every other Wealth Management business in the country, trust is at the epicentre of everything they do, reputational damage is very hard to repair (and quantify).

While the share price has taken a major hit and analysts have downgraded price targets aggressively, Citi for instance went from $8.65 to $4.50, Credit Suisse cut from $10.00 to $4.60 and Morgan Stanley from $10.80 to $5.00 - significant re-rates which shows how ‘wrong’ the market has been on this stock, digging into the downgrades, it’s more a function of increasing ‘risk premium’ being used than a big cut to earnings expectations. For example, consensus earnings per share before this latest news was around 67c however that number is now at 61c, a 10% downgrade at the earnings line but price targets as outlined above have been cut by around ~50%. Why?

IOOF (ASX:IFL) consensus earnings expectations (red) – share price (white)

Analysts may simply put a higher equity risk premium in their models given the obvious uncertainty and therefore that plays into a big downgrade of price targets, even though earnings have only moved a relatively small amount. This is important as it skews the p/e & yield numbers and makes them look attractive when they’re probably not. It also shows the fallacy of analyst’s in modelling and the benefit of using technicals and a dose of gut feel. Having sat through more presentations on stocks and more analysts briefings than I care to remember, I can say with some conviction that analysts can often get it very wrong, and they’re often slow to realise it.

Analysts may simply put a higher equity risk premium in their models given the obvious uncertainty and therefore that plays into a big downgrade of price targets, even though earnings have only moved a relatively small amount. This is important as it skews the p/e & yield numbers and makes them look attractive when they’re probably not. It also shows the fallacy of analyst’s in modelling and the benefit of using technicals and a dose of gut feel. Having sat through more presentations on stocks and more analysts briefings than I care to remember, I can say with some conviction that analysts can often get it very wrong, and they’re often slow to realise it.

IOOF (IFL) price to earnings ratio – exceptionally cheap on face value

From the above chart, IFL is now an exceptionally cheap stock if consensus earnings are achieved, however I bet if pressured analyst would simply have very little faith in their expected numbers – how could they when the situation is so fluid? The best on IFL was Laf from Bells who had been downbeat the name for some time. Looking forward, he now expects eps of 56.5c for 2019 dropping to 51.2c & 51.5c in 2020/21.

This is a lesson in looking at the numbers, but understanding the nuances behind them. When risk is too great, numbers become almost meaningless.

The one saving grace for IFL, and the reason why the dividend may actually be sustainable in the short term at least, is they raised ~$500m in new equity at $10.35 (plus arranged a $455m debt facility). If the acquisition does not go ahead, the debt facility will not be drawn plus they obviously have the equity that was raised to complete the deal. That could support the dividend or more likely, be used to buy back stock that would be strongly earnings accretive (sell at $10.35, buy back at $4.34 = good trade for IFL).

That is one positive in an otherwise disastrous situation, and it sets IFL in a better ‘relative’ position than AMP in our view. That said, at this point we have no interest in IFL nor AMP and reiterate the point we made back in June… Quite simply, we think there are too many variables for IFL.

From the above chart, IFL is now an exceptionally cheap stock if consensus earnings are achieved, however I bet if pressured analyst would simply have very little faith in their expected numbers – how could they when the situation is so fluid? The best on IFL was Laf from Bells who had been downbeat the name for some time. Looking forward, he now expects eps of 56.5c for 2019 dropping to 51.2c & 51.5c in 2020/21.

This is a lesson in looking at the numbers, but understanding the nuances behind them. When risk is too great, numbers become almost meaningless.

The one saving grace for IFL, and the reason why the dividend may actually be sustainable in the short term at least, is they raised ~$500m in new equity at $10.35 (plus arranged a $455m debt facility). If the acquisition does not go ahead, the debt facility will not be drawn plus they obviously have the equity that was raised to complete the deal. That could support the dividend or more likely, be used to buy back stock that would be strongly earnings accretive (sell at $10.35, buy back at $4.34 = good trade for IFL).

That is one positive in an otherwise disastrous situation, and it sets IFL in a better ‘relative’ position than AMP in our view. That said, at this point we have no interest in IFL nor AMP and reiterate the point we made back in June… Quite simply, we think there are too many variables for IFL.