What does the sell-off in bonds mean for traditional income stocks?

**This is an extract from the Market Matters Income Report from 17 September. Click here to get access to the full report and more

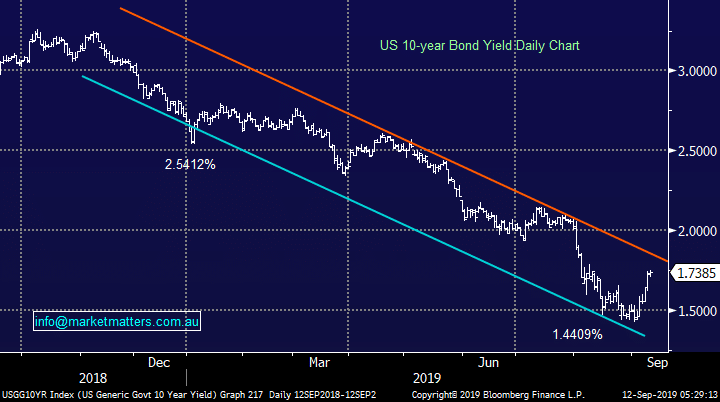

Over the past week we’ve seem reasonable activity across bond markets , with prices down and yields up, the US 10-year bond yield now trading at 1.73% versus a recent low of 1.44%. This has had obvious ramifications for traditional income stocks which have pulled back from highs generally set in early August. Sydney Airports(SYD) has declined around -8.5%, Transurban (TCL) is off more than -11%, Spark Infrastructure (SKI) -18% and Telstra (TLS) -11% excluding the August dividend of 8cps.

The obvious question being, should we be fading this bond market move, increasing our exposure to high quality income stocks into weakness?

The down trend in US & global bond yields has been aggressive in 2019 as many market followers now expect a recession in the next 12-months. President Trump’s approval rating has fallen below 40% following concerns on how he’s handling the US economy, around 60% of Americans now believe a recession is very likely hence the volatile President needs to resolve US – China trade sooner rather than later to kick start his 2020 election campaign - a potentially bullish outcome for bond yields.

However, bond yields have bounced numerous times in a broader downtrend only to fall away and make new lows. This time however the move has been a more aggressive one flying in the face of Donald Trump’s calls for rates to move lower.

On balance MM thinks US bond yields will at least test sub 1.5% one more time.

US 10-year Bond yield Chart

Assuming this is simply a short term spike in bond yields, it suggests that quality yield stocks can be bought into weakness, although at MM, we’re certainly less optimistic on the income stocks that are most influences by bond yields (i.e. infrastructure) given the maturity of the trend in rates.

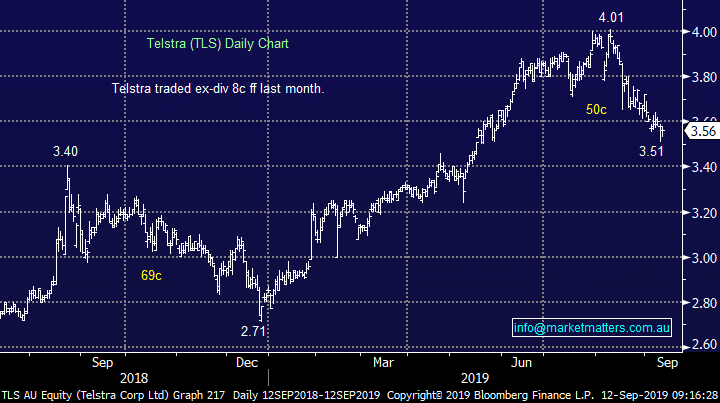

1 Telstra (TLS) $3.56 - forecast yield 4.5% ff

Telco heavyweight Telstra has enjoyed a strong 12 months trading from below $2.80 to briefly sneaking above $4 in early August. While the yield in Telstra has declined materially after they cut the dividend, this improves the sustainability of the payout while it should also improve the growth trajectory of the business.

MM views Telstra (TLS) as an accumulate between $3.45 & $3.60. with its 4.5% fully franked yield and lower payout ratio still attractive

Telstra (TLS) Chart

Assuming this is simply a short term spike in bond yields, it suggests that quality yield stocks can be bought into weakness, although at MM, we’re certainly less optimistic on the income stocks that are most influences by bond yields (i.e. infrastructure) given the maturity of the trend in rates.

1 Telstra (TLS) $3.56 - forecast yield 4.5% ff

Telco heavyweight Telstra has enjoyed a strong 12 months trading from below $2.80 to briefly sneaking above $4 in early August. While the yield in Telstra has declined materially after they cut the dividend, this improves the sustainability of the payout while it should also improve the growth trajectory of the business.

MM views Telstra (TLS) as an accumulate between $3.45 & $3.60. with its 4.5% fully franked yield and lower payout ratio still attractive

Telstra (TLS) Chart

2 Spark Infrastructure (SKI) $2.16 – forecast yield 6.94% unfranked

2 Spark Infrastructure (SKI) $2.16 – forecast yield 6.94% unfranked